Your paycheck feels bigger, but real purchasing power often isn’t — because inflation eats into wages faster than most Americans realize. This dynamic — influenced by Federal Reserve monetary policy, labor market trends, and everyday cost pressures — is quietly shrinking real take‑home pay and reshaping American financial life, especially for middle‑ and lower‑income workers. Data shows wage gains struggling to keep pace with rising prices over the long haul. (Visual Capitalist)

The Hidden Erosion of Your Paycheck

In recent years, inflation has silently infiltrated every aspect of American life. Prices for groceries, gas, rent, and healthcare have surged, often faster than wage growth. Millions of Americans now face a reality where their paycheck seems to grow — yet their actual financial comfort shrinks.

This isn’t just a perception. In real terms, inflation reduces purchasing power, meaning every dollar you earn buys less than it did a year ago. (Investopedia)

But the complexity doesn’t stop there. The Federal Reserve, through its monetary policy, indirectly influences both inflation and wage growth. Understanding this “silent battle” between your paycheck and inflation is crucial for protecting your finances.

What Is Inflation and Why Does It Matter?

Inflation is the increase in the average price of goods and services over time. When prices rise, the same amount of money buys fewer goods and services. This is why it’s essential to distinguish between nominal wages (your paycheck amount) and real wages (the purchasing power of that paycheck after inflation).

If your paycheck rises by 3%, but the prices of essential goods increase by 5%, your real income actually decreases. This is the invisible tax inflation levies on your everyday life. (Investopedia)

The Federal Reserve: The Invisible Hand Behind Inflation

The Federal Reserve, America’s central bank, doesn’t set prices directly. However, it plays a key role in managing inflation through monetary policy.

- Raising interest rates: Slows inflation by making borrowing more expensive, reducing spending.

- Lowering interest rates: Stimulates the economy but risks higher inflation.

For consumers, these actions affect mortgages, credit cards, car loans, and even job growth. While the Fed’s goal is to balance inflation and employment, the ripple effects are felt in every household budget.

Your Paycheck: Nominal vs. Real

Nominal wages may have increased in recent years, but real wages — wages adjusted for inflation — tell a different story.

Data Snapshot:

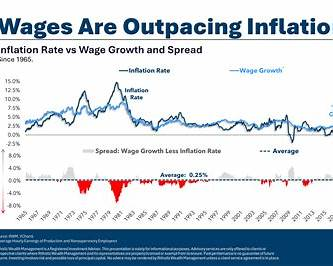

- From 2021 to 2025, consumer prices increased about 22.7% while wages only climbed 21.8%. (Visual Capitalist)

- Even Bankrate data shows that over four years, wage gains have not fully closed the inflation gap, leaving real purchasing power slightly below 2021 levels. (Bankrate)

The takeaway? Many Americans are earning more dollars, but those dollars don’t stretch as far as they used to.

Real-Life Examples of Inflation’s Impact

Example 1: Grocery Bills vs. Pay Raises

Sara from Ohio received a 3% pay raise this year. On paper, her income grew. In reality, her grocery bill jumped 7–10% due to rising food prices. Despite the raise, her budget buys less than before.

Example 2: Rent Surges Outpace Salaries

Marcus in New York earned a 4% salary increase after a promotion. Yet his rent rose by 6%, utilities increased, and commuting costs went up. While his paycheck increased, his financial breathing room shrank.

These examples highlight a harsh truth: nominal wage increases don’t always translate into better financial health.

Why Americans Are Feeling the Squeeze

Several factors contribute to the gap between wages and inflation:

- Slow Wage Growth

While wages have increased, growth hasn’t consistently outpaced inflation, leaving workers feeling the pinch. (Visual Capitalist) - Rising Living Costs

Inflation disproportionately affects essentials such as housing, groceries, healthcare, and transportation — items that consume large portions of household budgets. - Bracket Creep

Inflation can push individuals into higher tax brackets without a real increase in income, effectively lowering take-home pay. (Wikipedia) - Wage Stagnation Trends

Long-term wage stagnation means that even before recent inflation spikes, real incomes for many workers remained flat for decades. (Economic Policy Institute)

Trending Questions Americans Are Asking

1. Is inflation worse than wage increases?

Yes. Many workers find that even with raises, inflation reduces their purchasing power.

2. Why didn’t the Fed prevent this?

The Fed acts with a lag and cannot control supply chain shocks, energy price swings, or geopolitical events that impact prices.

3. Didn’t the economy add jobs?

Employment numbers are strong overall, but wage growth is slowing even as unemployment remains low. (Reuters)

4. Are real wages shrinking?

Yes. Inflation that outpaces nominal wage growth decreases real earnings, reducing actual purchasing power.

5. Which workers are hit hardest?

Lower- and middle-income earners feel the greatest pressure, as essential expenses take up a larger portion of income.

6. Is this permanent?

Not necessarily. Wage growth can catch up if labor markets tighten and productivity increases.

7. How does inflation affect savings?

Savings lose value if returns do not keep pace with inflation, eroding long-term wealth.

8. Should I adjust my finances now?

Absolutely. Budgeting, investing, and strategic planning are crucial to protect purchasing power.

9. Does everyone feel this same impact?

No. Geographic location, industry, and job type influence how much wage vs. inflation affects individuals. (Investopedia)

10. Can the Fed fix this alone?

No. Monetary policy works in tandem with fiscal measures, labor market dynamics, and global economic forces.

Actionable Takeaways for Workers

✔ Budget with inflation in mind: Track spending in essential categories such as groceries, housing, and utilities.

✔ Negotiate raises when possible: Aim for increases that at least match inflation.

✔ Diversify income and skills: Expanding your earning potential helps offset inflation pressures.

✔ Invest with inflation-protected instruments: Consider Treasury Inflation-Protected Securities (TIPS) or diversified investment portfolios.

✔ Monitor interest rates and loans: Rising rates affect mortgages, auto loans, and credit card debt.

Looking Ahead: What Could Change?

Economists project that real wage growth could improve if inflation stabilizes and labor markets tighten. Bankrate projects that the wage-to-inflation gap may fully close by 2026 if current trends continue. (Bankrate)

Global supply chains, fiscal policy, and energy markets will continue to influence inflation and wages, so it’s critical to plan proactively.

Conclusion

The silent attack on your paycheck is not a conspiracy — it’s the result of complex economic dynamics where inflation outpaces wage growth, affecting real purchasing power. Understanding how the Fed, inflation, and wage trends interact empowers Americans to take control of their finances. Budget wisely, invest strategically, and advocate for pay raises that reflect your true cost of living — only then can you truly protect your financial future.

Still Fit for Purpose?")